In economics, demand refers to the quantity of a commodity that buyers are willing and able to purchase at various prices during a given period of time. It’s not just a desire or need—a desire becomes demand only when supported by purchasing power and willingness.

For instance, wanting a car is a desire, but having the money and willingness to buy it makes it a demand. Thus, demand links consumer preferences with actual market transactions and forms the basis of all market analysis.

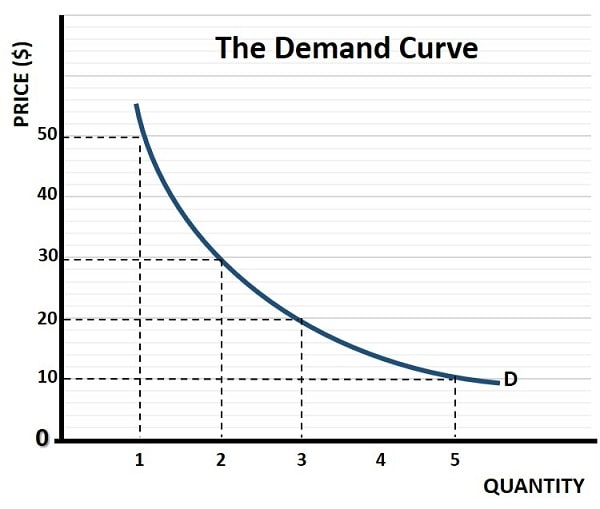

Demand Schedule

A demand schedule represents the relationship between price and quantity demanded of a good. It shows how much of a product consumers will buy at different price levels during a given period.

An individual demand schedule records how a single consumer responds to various prices, whereas a market demand schedule aggregates the demands of all consumers in a market.

Example: Demand Schedule for Rice in Tiruchirappalli Market

| Price of Rice (Rs/qtl) | Quantity Demanded (tonnes per month) |

|---|---|

| 950 | 5000 |

| 900 | 5100 |

| 850 | 5200 |

| 800 | 5300 |

| 750 | 5400 |

| 700 | 5500 |

The table clearly shows the inverse relationship between price and demand—as the price of rice decreases, the quantity demanded increases, illustrating the Law of Demand.

Determinants of Demand

The level of demand for a commodity depends on various economic and social factors. The major determinants of demand are as follows:

1. Tastes and Preferences of Consumers

Changes in fashion, trends, and advertising campaigns influence consumers’ preferences. For example, increased awareness of healthy eating can raise the demand for organic products.

2. Income of the People

There is generally a positive relationship between income and demand. As people’s income rises, they tend to buy more goods and services, while a fall in income reduces demand.

3. Price of the Commodity

The price of a commodity directly affects its demand. When prices rise, demand falls, and when prices fall, demand increases—assuming other factors remain constant. This is the foundation of the Law of Demand.

4. Prices of Related Goods

Demand is influenced by the prices of substitute and complementary goods:

- Substitutes: When the price of tea falls, consumers may buy more tea and less coffee.

- Complements: A fall in the price of milk raises not only milk demand but also the demand for sugar, since they are consumed together.

5. Population

An increase in population leads to higher overall demand for goods and services, while a declining population can reduce market demand.

6. Income Distribution

If income is evenly distributed, demand for basic goods rises. In contrast, if income is unequally distributed, demand for luxury items tends to be higher among the wealthy class.

7. Expectations about Future Prices

When consumers expect prices to rise in the future, they tend to buy more now, increasing current demand. Conversely, expectations of falling prices may delay purchases.

Economic Insight

Demand is one of the most fundamental concepts in microeconomics. It helps economists and policymakers understand consumer behavior, price formation, and market equilibrium. Without demand, production decisions, pricing strategies, and economic planning would lose direction.

Conclusion

Understanding demand in economics is essential for analyzing how consumers react to price changes and economic trends. It bridges the gap between consumer behavior and market supply, shaping the overall economic structure. For B.Sc. Agriculture and B.V.Sc. & A.H. students, mastering demand theory builds the foundation for analyzing production, pricing, and policy implications in real-world markets.

Explore more economics concepts on Pedigogy.com, Nepal’s leading platform for research-based education in agriculture and veterinary sciences. Visit our Economics section here.

Updated on 8 November 2025