Economics is the science that studies how people produce, exchange, and consume goods and services within different systems. It explains how limited resources are used to maximize wealth and human welfare. The heart of economics lies in scarcity and choice — since resources are limited, individuals and societies must choose the most efficient way to use them.

For instance, a farmer may have to decide whether to grow paddy, sugarcane, or banana depending on the availability of irrigation water. This need for decision-making due to scarcity makes economics an essential study for understanding how we allocate resources efficiently.

Two key factors create economic problems:

- Unlimited human wants

- Scarcity of available resources

Thus, economics examines how to satisfy countless human wants with limited means. It links want, effort, and satisfaction, shaping both personal and national welfare. It also studies broader aspects such as national income, public finance, and international trade.

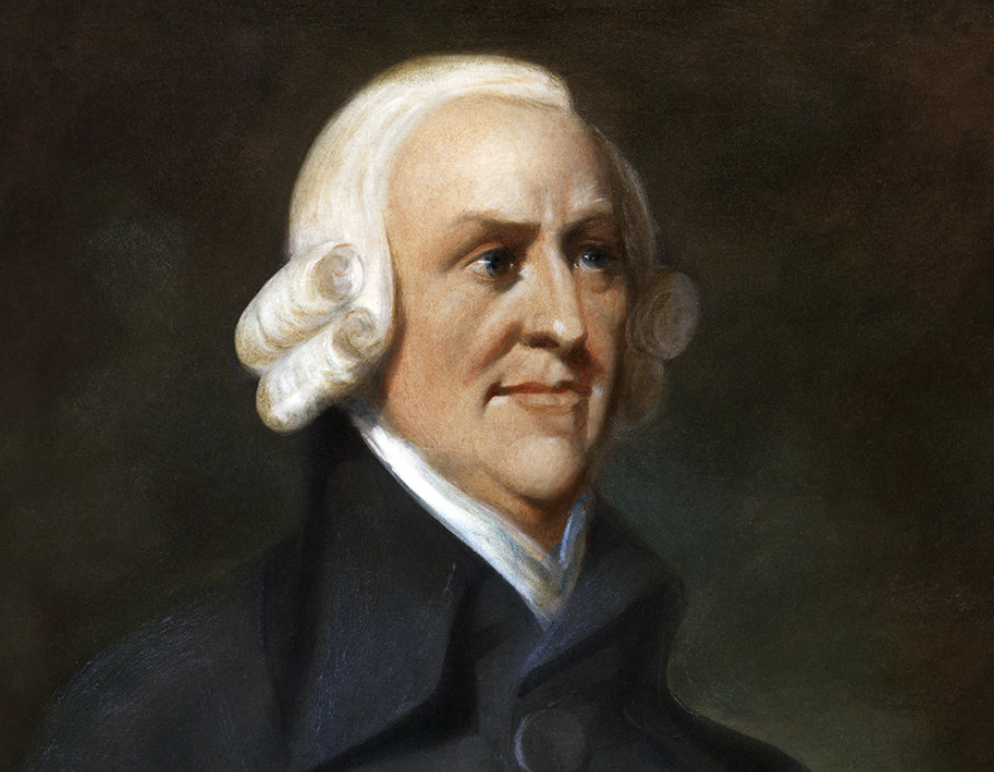

I. Adam Smith’s Definition of economics – The Wealth Definition

The foundation of modern economics was laid by Adam Smith (1723–1790) in his famous book “An Inquiry into the Nature and Causes of the Wealth of Nations” (1776).

According to Smith, economics is the science of wealth. He believed that individuals working for their self-interest ultimately promote the welfare of society, guided by what he termed an “invisible hand.”

Criticisms:

- Smith’s definition focused only on wealth, not on human welfare.

- Critics like Ruskin and Carlyle called economics a “dismal science” because it seemed to encourage selfishness.

- Later economists emphasized that wealth is only a means, and human welfare should be the ultimate goal.

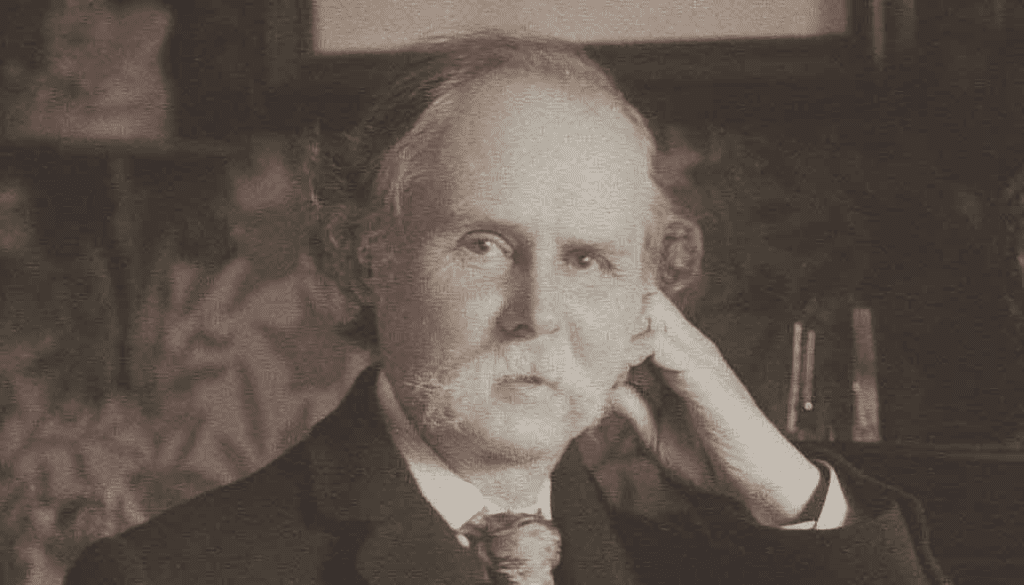

II. Alfred Marshall’s Definition of economics – The Welfare Definition

Alfred Marshall (1842–1924) refined the scope of economics in his book “Principles of Economics” (1890). He defined economics as:

“A study of mankind in the ordinary business of life; it examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requisites of well-being.”

Key Features of Marshall’s Definition:

- Economics studies human welfare and economic activities in daily life.

- It considers both individual and social actions related to material well-being.

- Marshall distinguished between material goods (tangible) and immaterial goods (intangible), focusing mainly on the former.

Criticisms:

- Marshall ignored immaterial goods such as education and healthcare, which also promote welfare.

- His definition limited economics to material welfare, which varies across time, culture, and individual perception.

- Welfare cannot be precisely measured, making it an unclear foundation for economics.

Despite its flaws, Marshall’s welfare approach made economics more human-centered, moving it beyond the narrow idea of wealth.

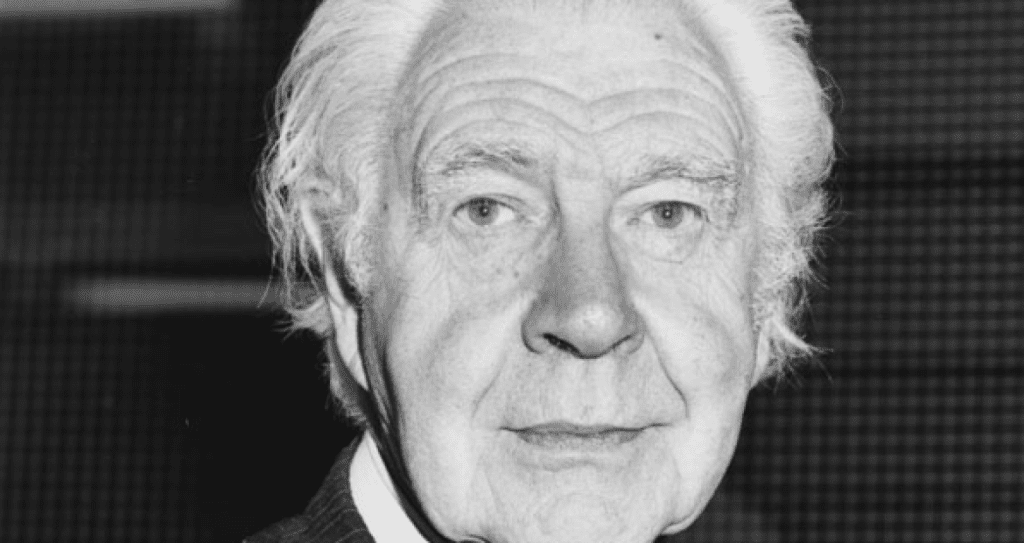

III. Lionel Robbins’ Definition of economics – The Scarcity Definition

Lionel Robbins (1898–1984) revolutionized economic thought with his book “An Essay on the Nature and Significance of Economic Science” (1932).

He defined economics as:

“A science which studies human behavior as a relationship between ends and scarce means which have alternative uses.”

Key Features of Robbins’ Definition:

- Ends = unlimited human wants

- Means = limited resources

- Scarcity forces individuals to make choices between alternatives

Thus, economics, according to Robbins, is a science of choice under scarcity.

Merits:

- Robbins gave economics a more scientific and analytical foundation.

- His definition applied to all human behavior involving choice, making it universal.

- It separated economics from moral judgments, focusing purely on decision-making.

Criticisms:

- Robbins ignored the ethical and welfare aspects of economics.

- He treated all wants equally, whether good or harmful (e.g., rice vs. alcohol).

- His definition excluded macroeconomic issues like growth and national income.

Despite criticisms, Robbins’ theory remains influential, emphasizing that economics is about how people make choices when resources are limited.

Conclusion

The concept of economics has evolved from the study of wealth (Smith) to welfare (Marshall) and finally to scarcity and choice (Robbins). Together, these definitions explain that economics is not just about money but about human behavior, decision-making, and welfare.

In essence, economics helps us understand how to make the best possible use of scarce resources for maximum welfare — both for individuals and societies.

Explore more economics concepts on Pedigogy.com, Nepal’s leading platform for research-based education in agriculture and veterinary sciences. Visit our Economics section here.

Updated on 5 November 2025