Depreciation

- The decrease in the value of any equipment due to the wearing and tearing over the time is called as depreciation.

- It represents the amount by which a farm resource decreases in value, as a result of cause other than a change in the general price of the item.

Methods of calculating depreciation

- Annual Revaluation:

- This is the yearly valuation of assets. This method implies estimating the market value of the asset in the beginning and the end year inventory and then taking the difference as depreciation.

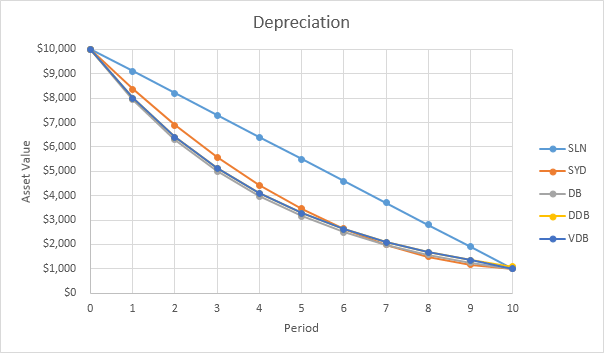

- Straight line method:

- This method is easy, simply and usually most satisfactory for most various purposes.

- From this method, the annual depreciation of assets is computed by dividing the original cost of the assets less salvage value by the expected year of life.

D=OC-SV/EC

Where, D = Depreciation

OC = Original Cost

SV = Salvage value

EC = Expected Life

- This method is more useful for durable assets like building and fences that may require uniform maintenance during their lifetimes.

- Double declining balance method:

- Fixed rate depreciation is used every year and applied to the remaining value assets at the beginning of each year.

- It is important to note that salvage value is not subtracted from the original cost as in the various methods.

- Sum of the year digits or reducing fraction method:

- The following formula is used for calculating the annual depreciation

AD = F*AMD

Where,

AD = Annual Depreciation

F = Fraction

AMD = Amount to be depreciation

F = RM/SYM

Where,

F = Fraction for any year

RM = Year of remaining life at the beginning of account period

Problems in Calculating Depreciation

1.The life of many machines is often longer than the normal expectations.

2.In case of minor repair, use of oil and lubrication, etc. normally no extra depreciation is charged. If, however, machines are reconditioning or buildings are repaired or remodeled to an extent to appreciably increase their value within the accounting year. A convenient procedure is to add the cost of the repairs to the existing value of the asset.

3. In case of small tools, they are considered to be used up within one year. Assume 100% depreciation on them.

4. If machine is purchased as second hand, the number of the years it has been used and the original price may not be known, the logical procedure in this case is to estimate the remaining years of its life and begin depreciation on the purchase price.

5. When the livestock is in breeding stage or appreciation phase, revaluation method will be more useful. But, when they start depreciating say after 3rd year, in case of bullocks, straight-line would be appropriate.